Easy Wins in Low Latency Market Data Feed Parsing

how to wire up a bba feed parser in cpp to your python application for fast wins

It turns out that an incredible number of quantitative trading firms run on Python. When we think about quant trading, we often only talk about the Citadel-s and Optiver-s, but particularly in the crypto space - the biodiversity is rich and competition is variable. The animals in the canopy and those in the shrubs thrive on a different diet.

One of the things I like to do when my friends hop firms is to ask what the focus of the interview was, the skills involved et cetera. I was rather surprised that Python still has a good seat in the software stack of crypto trading firms, and not in the “dashboard and risk” layer. In the actual trading logic.

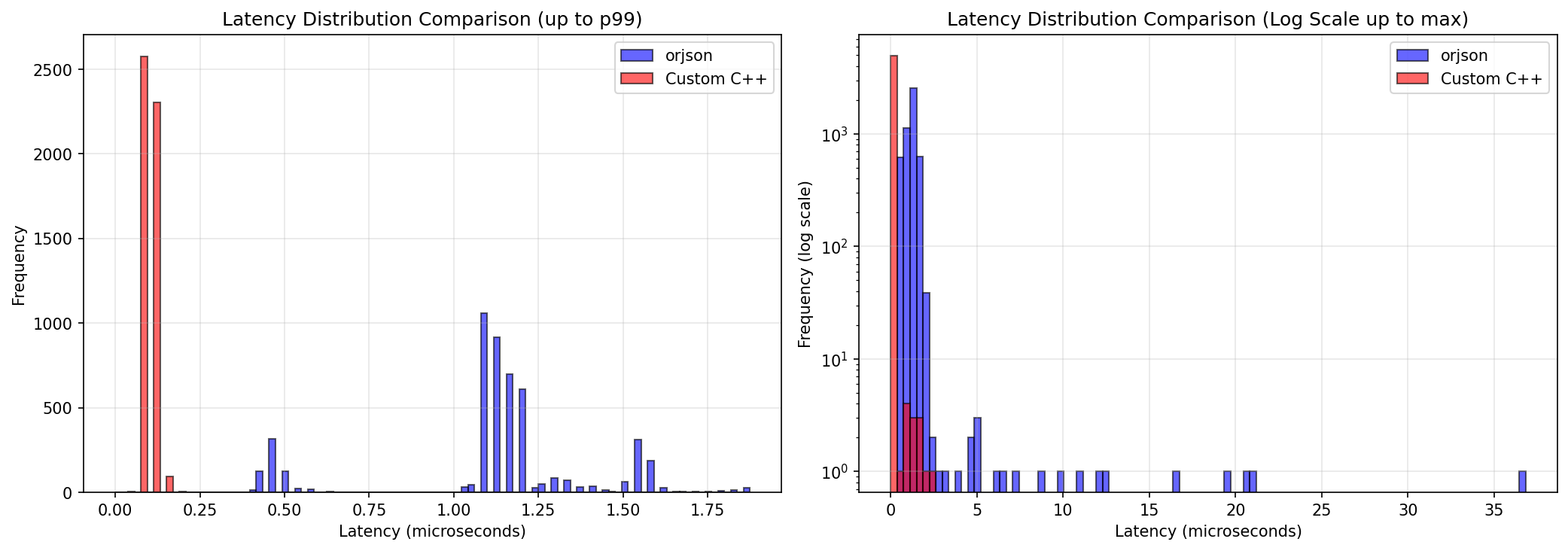

Anyways, I did come across scenarios for my own (low latency) trading purposes, where I wanted to optimise feed parsing but the entire system was written in Python. It is a pretty neat trick, the gains are nice (~10x), use case is diverse and implementation is simple - fantastic to share.

Let’s go!