FORMULAIC ALPHA REPORT

In the previous post, we looked at the basics of using a quadratic optimizer in Python to implement portfolio optimization with long constraints and cost-aversion.

In the next research post, we look further into the problem of cost penalization. We look at the cost of miscalibrating parameters in the loss function. We extend the N asset problem into the N alpha problem, which affects our constraint matrices and objective functions, the difference being that turnover is penalized on an underlying implied portfolio rather than the alpha weight distance. We show code. We then look at robust methods for estimation of the covariance matrix.

In the market notes, we introduce chapters on exotic and american derivative pricing.

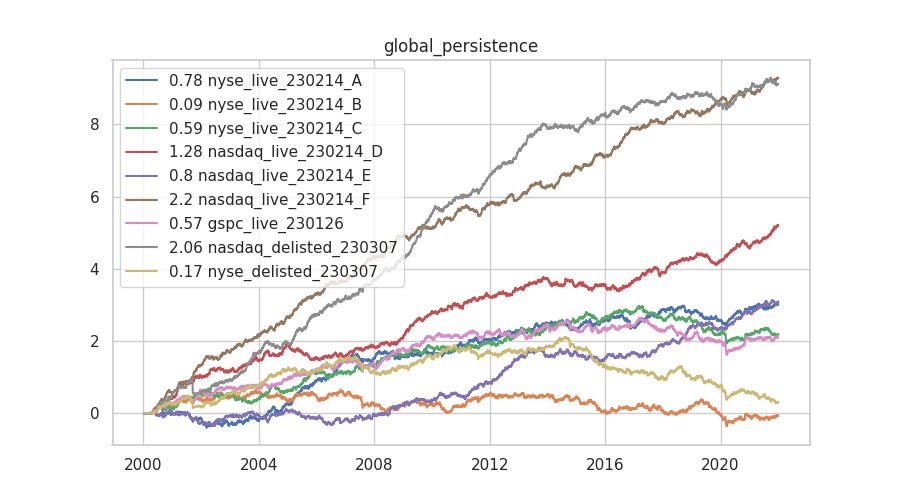

Log Returns Preview (sharpe dataset_name)

Alpha Report (paid readers)