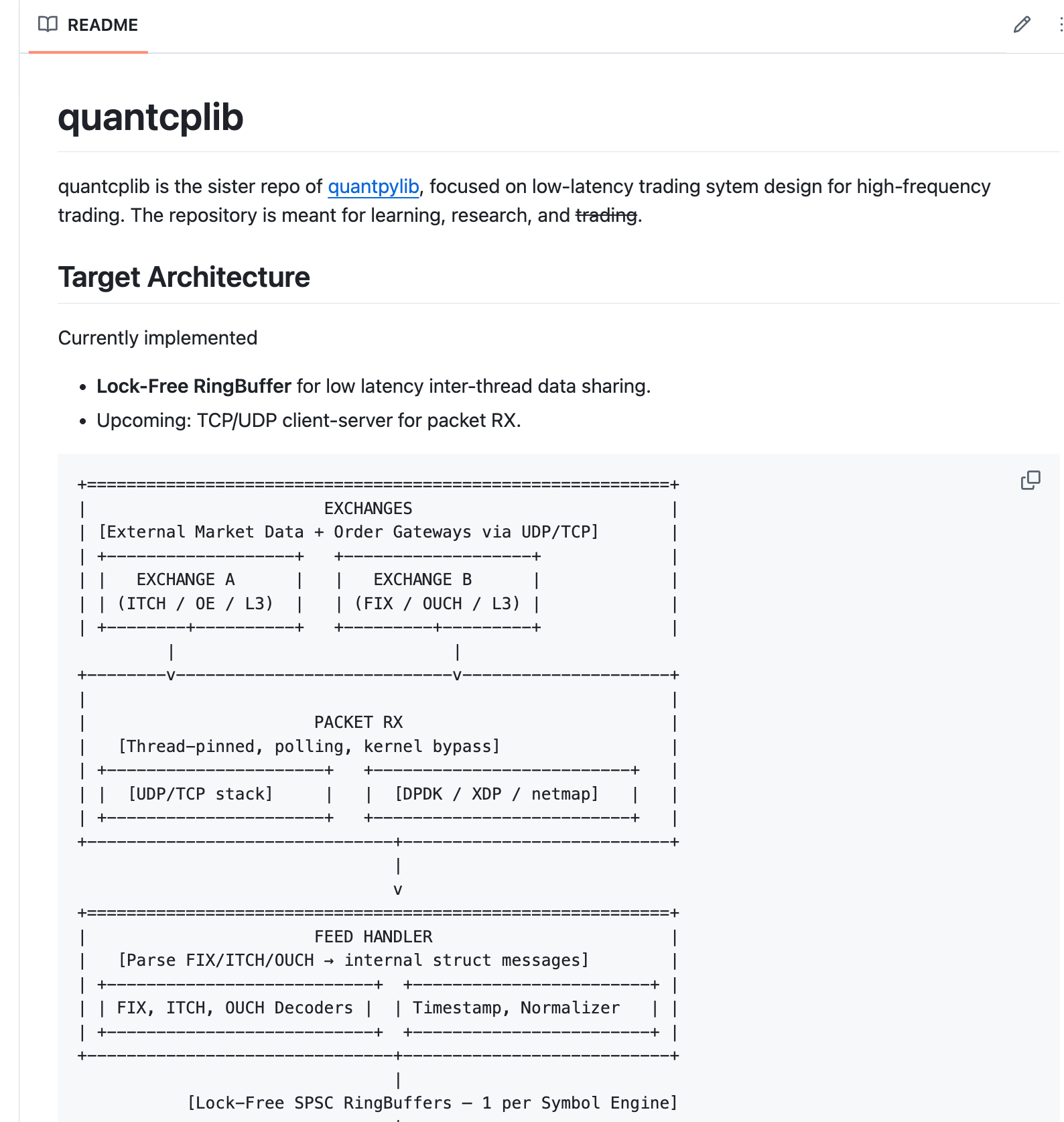

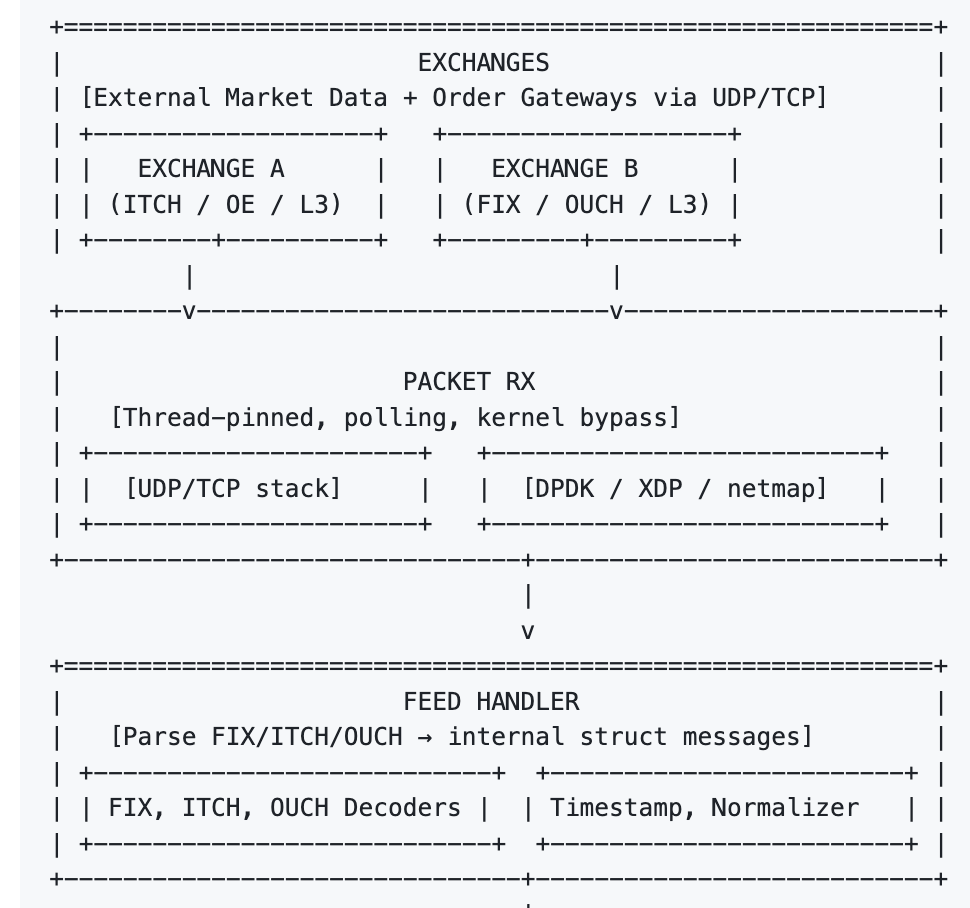

HangukQuant quantcplib Github Repo

As you know, quantpylib is our Python Github repo designed for learning, research and trading. It has features for exchange integration, quantitative backtesting, exchange simulations, regression libraries, event-driven trading and more.

As of today, it supports ‘low’ latency trading through event-loop based co-operative multitasking using the async-paradigm supported by Python.

I am excited to announce quantcplib - a dedicated cpp library designed for learning, research and trading, with design choices focused on ultra-low latency trading system design.

As of today - it is not ready for trading, but we will be expanding out the repository, code examples and features as we forage through low-latency trading concepts.

For a preview of the kind of work we will be exploring, I have open-sourced implementation of the cpp port for a low-latency inter-thread data sharing framework, the ‘LMAX Disruptor’:

https://github.com/hangukquant/disruptor_cpp/

All subscribers have access to the Github repo, as do anyone who currently has a repo pass to quantpylib. There is no separate pass to obtain access. Official documentation page will be hosted soon.

Given the ‘greenfield’-ness of the project and the cpp expertise of yours truly, we will also accept requests for admission on case-case basis, presupposing some cpp experience, willingness to contribute, guide and critique. Special requests by email only.

For subscribers, just comment your GH username, which I’ll remove once done.

Cheers!

C++, things are getting serious 🫡

can I cpp :D