Manage Your Quantitative Tick Data Lake with Quantpylib

In the last post, we discussed what institutional data capture needs to preserve and how to design a clean architecture for maintaining your own data lake for quantitative research.

This is available in quantpylib, our quant repo for annual, paid subscribers:

We have redesigned critical core architecture and subsystems that will enable powerful workflows for traders using quantpylib in their trading infrastructure. Examples include performant and institutional-grade data replay, event journaling, telemetry systems and quantitative analytics.

We are proud to announce that managing your data lake has been now made a ~100~ lines of code powered by quantpylib, into raw binary flat files.

We have also shipped and documented a bunch of improvements to our backend, including cpp implementations for native orderbooks states. Once we launch versioning, we will deprecate old APIs.

See our data archival example here:

https://quantpylib.hangukquant.com/hft/hft/#data-archival

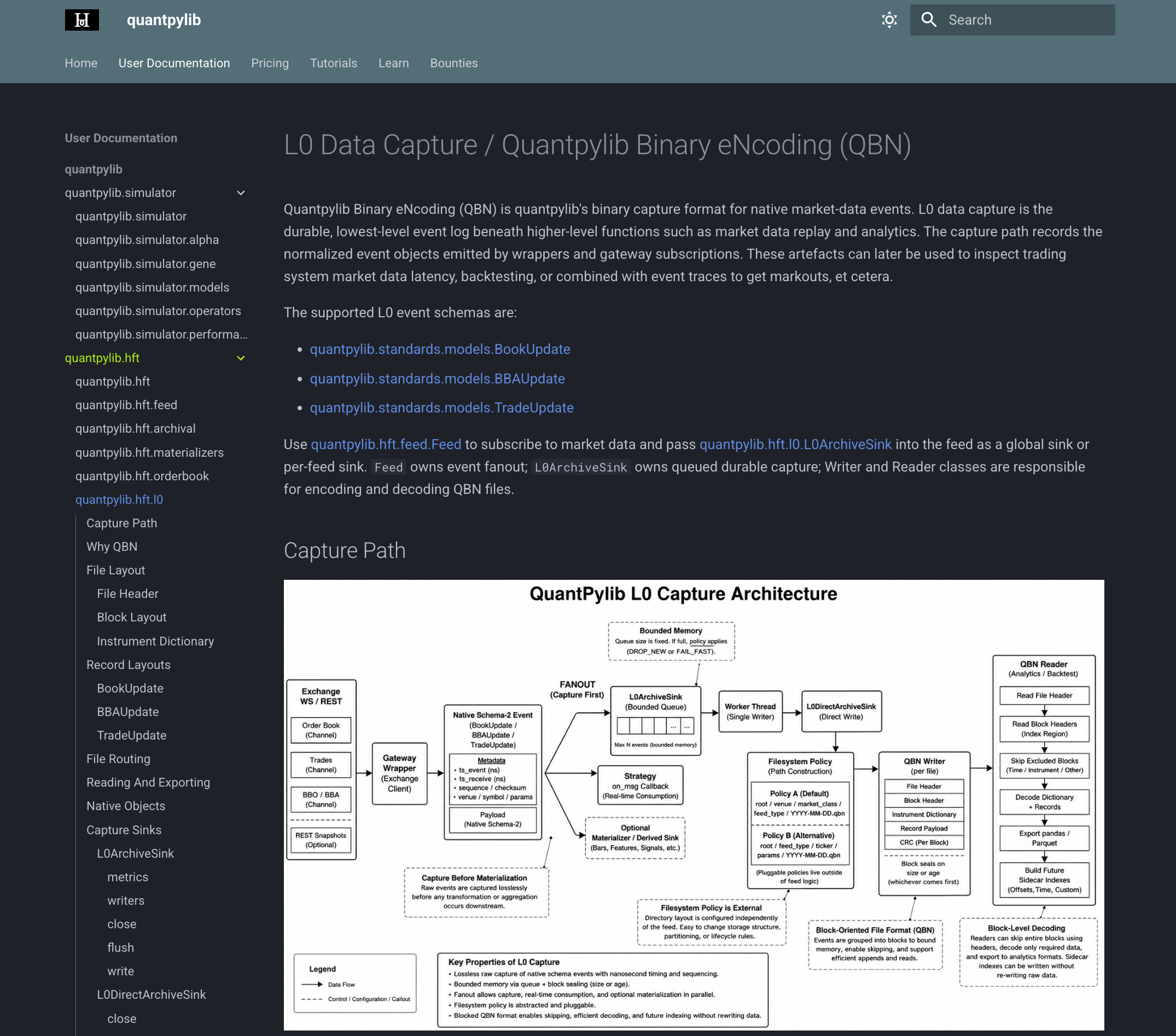

See our feed model and QBN encoding notes:

https://quantpylib.hangukquant.com/hft/feed/

https://quantpylib.hangukquant.com/hft/l0/

Our new, performant native orderbook implementation is documented here:

https://quantpylib.hangukquant.com/hft/orderbook/

We continue our aim of providing institutional grade trading infrastructure available to serious traders.