Primer on Volatility Estimators

In our last market notes, we ran through some fundamentals in option theory:

In this post we will run through some popular volatility estimators, such as the

close-to-close Estimator

Parkinson Estimator

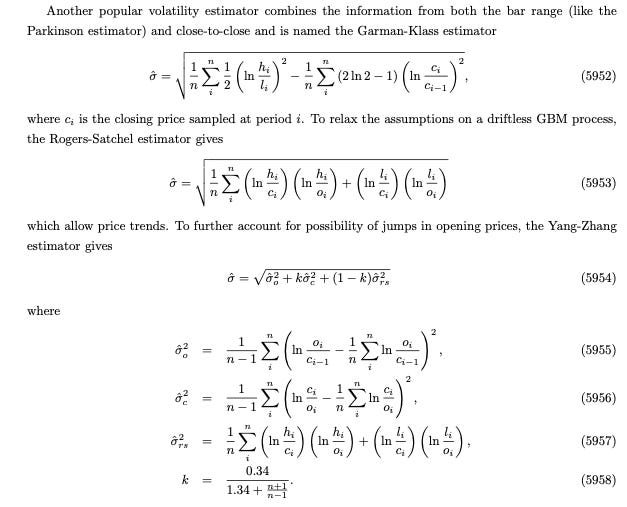

Garman-Klass Estimator

Rogers-Satchel Estimator

Yang-Zhang Estimator

Preview:

Download the notes here:

In the next post, we will implement the code for these estimators and try them out on SPY data. Code will be released to paid readers only.

Upcoming posts (1-2 weeks):

Implementation of volatility estimators

Formulaic Alpha report

Convex optimization notes

Options backtesting code

This is the full market notes, so that you can use a pdfviewer and conveniently jump to the references: (paid)