Quantitative Trading Strategies - How I went from 10k to 100k to 1M (new series intro)

uncovering some of the dirty work

Not too long ago, I ran the nimble market-maker series, discussing important techniques for quants in pseudo-competitive trading environments.

We developed a number of critical tips and tricks there that the quantitative trader should be aware of when profiling and deploying trading strategies. It was very well received, and a reader even changed their username to thenimblemm 😅

I’ve been writing this blog for 5 years now, and over the years - we focused mainly on developing quantitative research frameworks - on the how rather than the what. Here and there, we discussed some quantitative strategies, which talk about the what.

After half a decade, I thought it would be a nice series to give some more detail into WHAT goes on behind the scenes in my ‘dirty operations’.

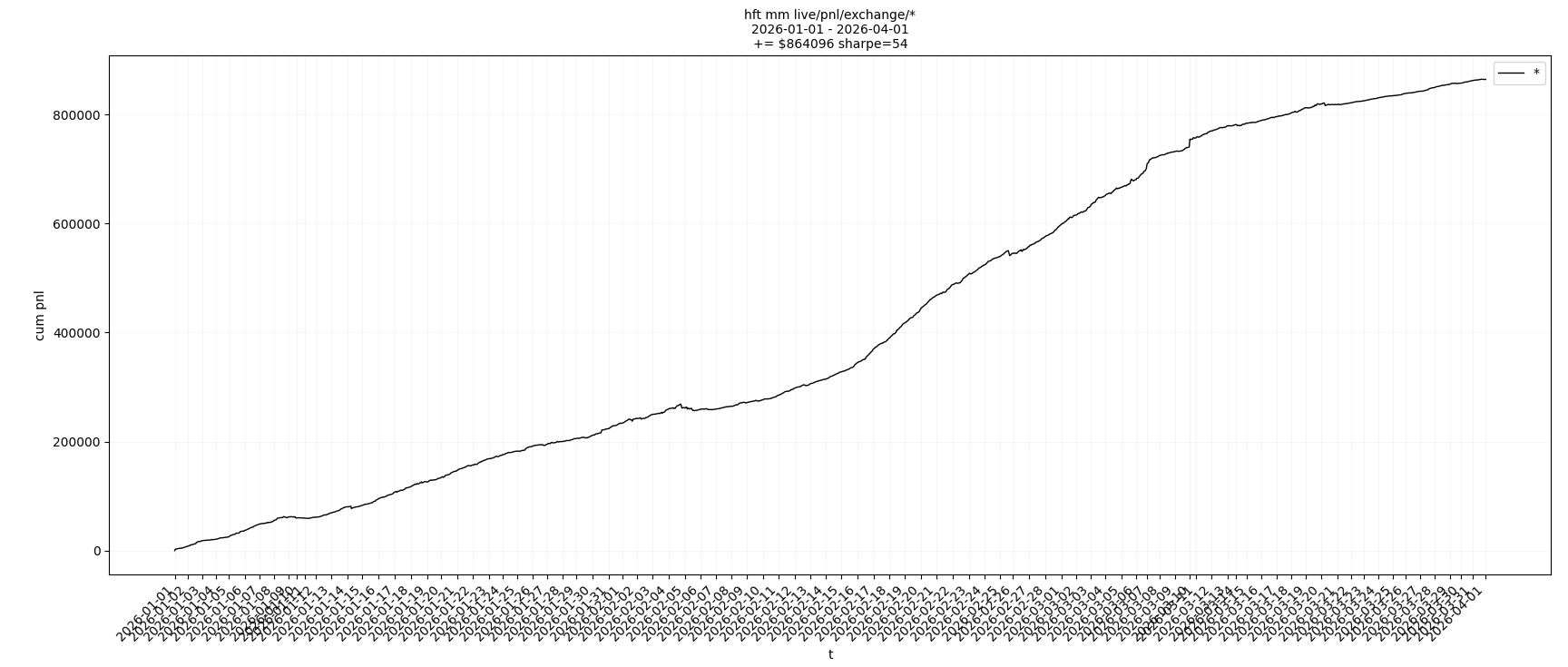

From trend following, to factor trading, FX policy arbitrage, event driven trading, to cross-exchange statistical arbitrage and hft market making - these 5 years was a busy one!

7 Days Discount

For 1 week, all subscription plans are 50% off:

https://www.research.hangukquant.com/d7b4564d

You can also support me with a Lifetime Subscription here:

https://buy.stripe.com/dRm3cw0mC05N6Am3XKe7m0f

Shout out to the ~300 lifetime members who have supported me, love ya back.

Hope you look forward to the series!