Statistical Suites with Russian Doll System (IMPORTANT!)

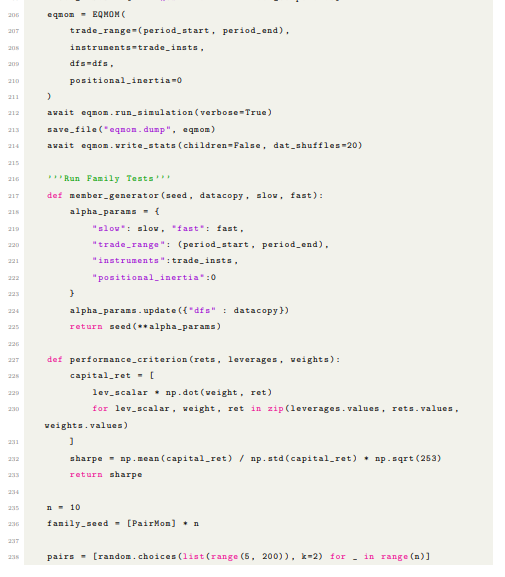

The Russian Doll system is our core proprietary backtesting engine designed for trading multi-instrument and multi-strategy frameworks. It can be thought of as a culmination of the topics we discussed so far on our papers, incorporating logic for execution costs, positional inertia, volatility targeting, risk management, fill sensitivity, inter-currency trading mechanisms, vector trading, asynchronous trading and statistical hypothesis testing.

We are glad to finally release an updated version of the Russian Doll backtesting engine, which now contains statistical hypothesis testing for active management ability. The relevant theory on the discussion of statistical hypothesis tests were discussed here:

A portion of the paper with code is made available to all readers:

Preview:

Here is the full paper (50 pages) for readers and source code files for download (paid readers):