QUANT LECTURE RELEASE -

Some ornamental points:

as promised, we have started sending out invitations for the cpp Github repo,

targeted for low latency trading. We will build this out over the coming year, and will dive into each component thoroughly. How-to for the invites are in the post.

our essentials for quant trading lecture discounts are closed;

upcoming posts: detailed review of disruptor pattern, analysis > quant handbook, measure theory > quant handbook, writing a TCP client for packet RX using io_uring/epoll to reduce syscalls and kernel arbitrations.

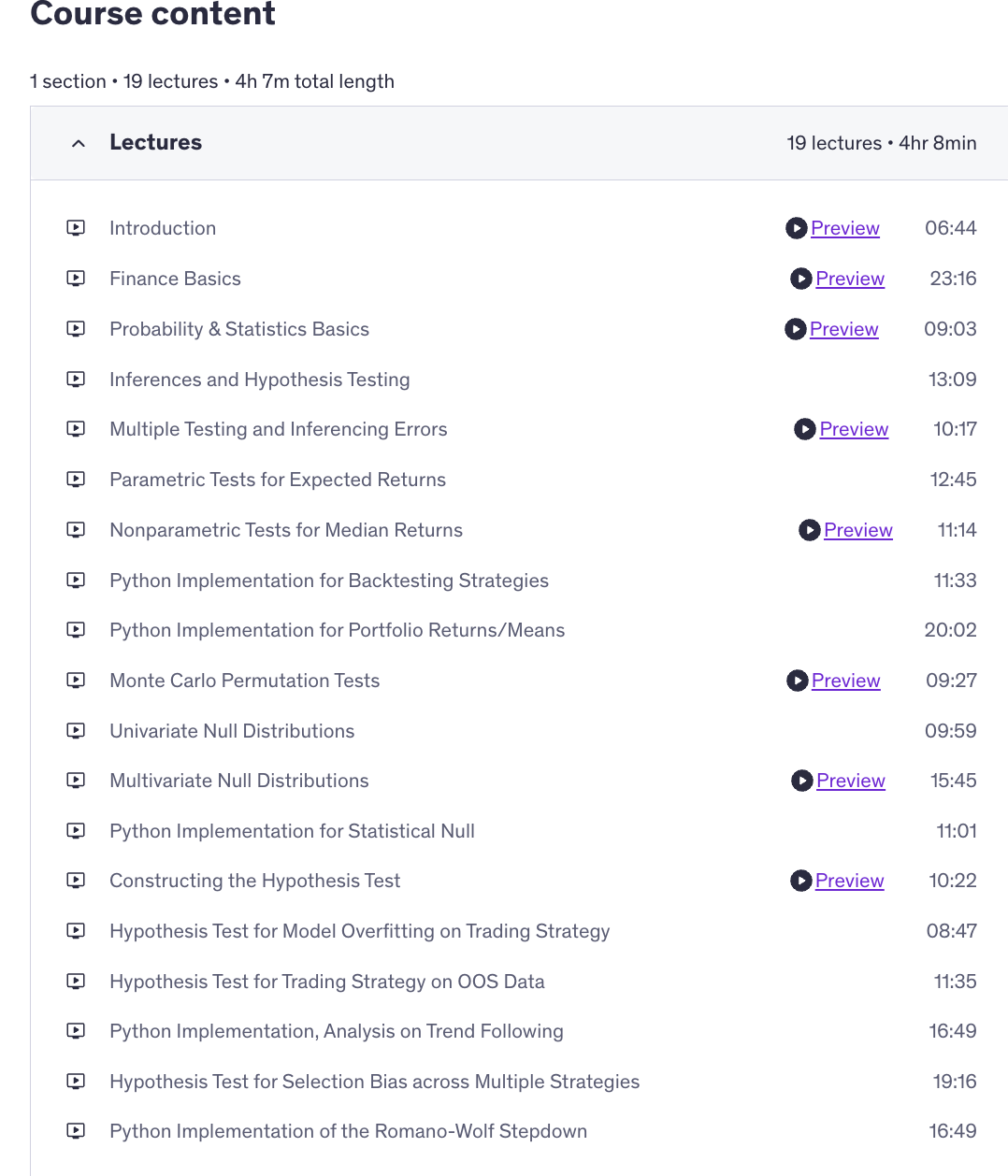

new lectures are released!

I’ve taken great effort to explain from foundational probability theory up to nontrivial, advanced statistical sampling procedures to construct useful tools for validation in quantitative trading problems, with Python implementations and modifications under practical constraints.

I have placed it at max discount on this link for 5 days.

For lifetime thinkific - I have/will send out a free view link.

Rest of the subscribers, please fill out the reviewer access link below if you are interested.

TOC:

Reviewer access link: